In the dynamic landscape of financial technology, Spydra emerges as a trailblazer with the introduction of the Open Credit Enablement Network (OCEN) Framework. This revolutionary initiative stands at the forefront of transforming credit enablement, offering a standardized and open infrastructure that fosters innovation, collaboration, and transparency. As we delve into the intricacies of Spydra's OCEN Framework, we unveil a paradigm shift in the way credit solutions are approached, addressing industry challenges and paving the way for a more interconnected and efficient credit ecosystem. Join us on this journey as we explore the transformative power of Spydra's OCEN Framework in revolutionizing credit enablement.

Understanding OCEN: Unveiling the Future of Credit Enablement

In the ever-evolving landscape of financial technology, the Open Credit Enablement Network (OCEN) stands as a beacon, ushering in a new paradigm of credit enablement, empowerment, and collaboration. More than just a framework, OCEN represents a transformative force that addresses longstanding challenges within the credit ecosystem.

What is OCEN?

At its core, OCEN is a standardized and open infrastructure designed to revolutionize the credit landscape. It provides a common framework for financial institutions, fintech companies, and various stakeholders, breaking down silos and fostering a collaborative environment.

The Technical Foundation: Hyperledger Fabric and Spydra's Integration

OCEN finds its technical foundation in the robust Hyperledger Fabric framework. Spydra Technologies, a pioneer in blockchain solutions, plays a crucial role in elevating OCEN through seamless integration on its private blockchain network. This not only ensures security but also facilitates a user-friendly experience for participants.

The Role of Blockchain: Transparency and Reliability

In a landscape where data integrity is paramount, OCEN leverages blockchain technology to establish a transparent and reliable foundation. The blockchain's immutable ledger ensures the accuracy of shared data, providing a single source of truth for all participants. This not only enhances transparency but also fosters trust among collaborators.

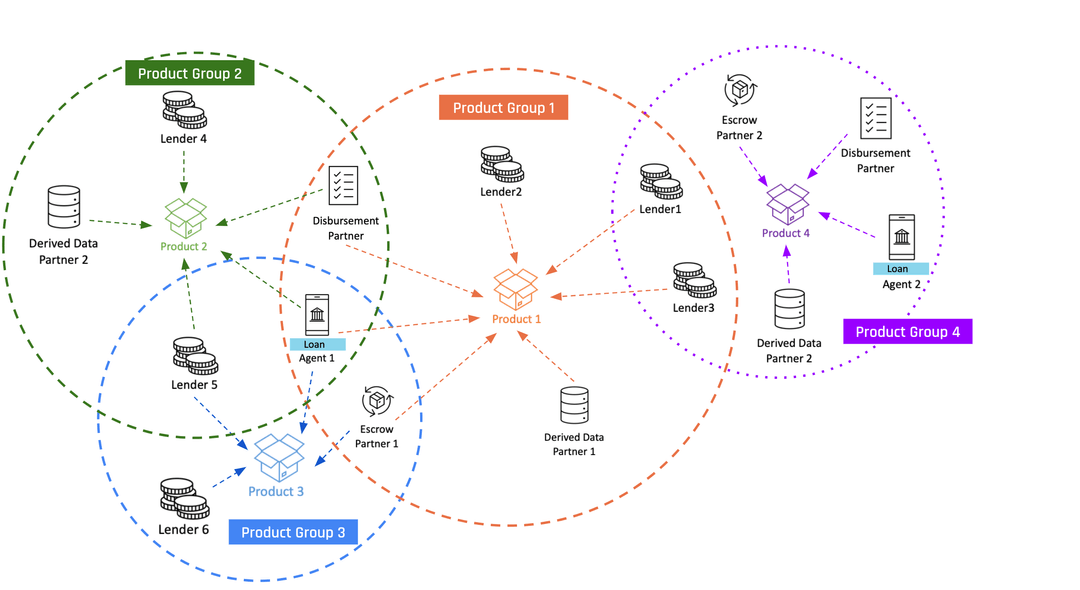

Key Participants in the OCEN Ecosystem

OCEN thrives on collaboration, and its participants play distinct yet interconnected roles in this revolutionary network:

Lenders: The architects of loan products, driving innovation in credit solutions.

Loan Agents: Advocates for borrowers, facilitating the loan process and selecting the best offers.

KYC Partners: Technology experts collaborating with Loan Agents for Assisted KYC.

Disbursement Partners: Facilitators of Purpose Controlled products, ensuring seamless payments within the OCEN journey.

Collection Partners: Collaborators aiding in the collection process, enhancing flexibility for lenders.

Derived Data Partners: Providing supplementary data, enriching lenders' underwriting engines with valuable insights.

OCEN & Spydra: A Synergy of Innovation

Spydra has gone above and beyond in simplifying the adoption of OCEN on the blockchain, ensuring seamless integration and unparalleled security.

Private Network on Hyperledger Fabric

Our private blockchain network, built on Hyperledger Fabric, facilitates the onboarding of multiple participants, including Loan Agents, Lenders, and other key roles. This ensures a secure and efficient environment for credit enablement.

Data Encryption and Privacy

Object and field-level encryption allows selective sharing of data between participants within the same product network. Participants retain control over what information is stored on the ledger, ensuring data privacy and security. Different Fabric channels for each product network provide additional isolation, enhancing security.

Configurable No-Code Workflows and Oracle Integration

Spydra's platform offers configurable no-code workflows, empowering users to create smart contracts for critical processes effortlessly. This includes processes such as loan repayment, approvals, conditional disbursement, and KYC checks. Additionally, the integration of oracles allows the retrieval of external data, such as KYC information, during smart contract execution.

We are not just adopting OCEN on the blockchain; we are elevating it to new heights of efficiency, security, and user-friendly integration. As we continue to reshape the landscape of credit enablement, we invite you to explore the limitless possibilities that OCEN on Spydra's blockchain brings to the table.

Challenges Addressed by OCEN

OCEN tackles critical challenges within credit enablement:

Fragmented Data: Standardizing integration creates a unified platform, overcoming the challenge of fragmented information.

Lengthy Processes: Leveraging smart contracts automates business processes, ensuring faster and more efficient workflows.

Lack of Interoperability: OCEN promotes interoperability, bridging gaps between financial institutions, fintech companies, and stakeholders.

Disputes Over Shared Data: The transparent and immutable nature of the blockchain reduces disputes, establishing trust among participants.

Challenges in Credit Enablement Today

Fragmented Data:

Challenge: Traditional credit models often face the hurdle of fragmented and siloed data, making it challenging to create comprehensive and accurate credit assessments.

Solution with OCEN: OCEN standardizes integration, creating a unified platform where participants seamlessly share data. The blockchain's immutable ledger ensures the reliability and integrity of this shared information, overcoming the challenge of fragmented data.

Lengthy Processes:

Challenge: Cumbersome, time-consuming processes hinder the efficiency of credit enablement, leading to delays in loan approvals and disbursements.

Solution with OCEN: OCEN leverages smart contracts to automate business processes and rules, streamlining workflows based on predefined conditions and triggers. This eliminates the need for a single enforcement party, ensuring faster and more efficient execution of credit-related processes.

Lack of Interoperability:

Challenge: Traditional credit ecosystems often lack interoperability, making it difficult for different participants to collaborate seamlessly.

Solution with OCEN: OCEN is designed to bridge this gap by promoting interoperability and collaboration between financial institutions, fintech companies, and various stakeholders. It establishes a standardized and open infrastructure, breaking down silos and fostering a more interconnected credit ecosystem.

Disputes Over Shared Data:

Challenge: Disputes arising from differences in documentation or disagreements over shared data can hamper the credit assessment and lending processes.

Solution with OCEN: The transparent and immutable nature of the blockchain ensures a single source of truth for all participants. This significantly reduces disputes by providing a clear record of shared data, fostering trust and collaboration.

Multiple Integrations:

Challenge: Traditional credit networks often require participants to undergo multiple integrations for different product networks, adding complexity and inefficiency.

Solution with OCEN: A blockchain network simplifies processes, eliminating the need for multiple integrations. Participants involved in multiple product networks can seamlessly operate within the OCEN framework, reducing the complexities associated with integration.

Data Privacy and Security Concerns:

Challenge: Concerns regarding data privacy and security are paramount, especially in the financial sector.

Solution with OCEN: OCEN, implemented on a private blockchain network, ensures data encryption at object and field levels. Participants have control over what information is stored on the ledger, enhancing data privacy and security. Different Hyperledger Fabric channels for each product network provide further isolation, fortifying the overall security framework.

Lack of Flexibility in Underwriting Models:

Challenge: Traditional credit systems often struggle with the lack of flexibility in adapting to new underwriting models based on evolving data sets.

Solution with OCEN: Derived Data Partners within the OCEN network furnish supplementary data to lenders, aiding in enhancing underwriting engines with additional information. This allows for greater flexibility, enabling lenders to create new underwriting models based on fresh and diverse data sets.

Benefits of OCEN Adoption

The adoption of OCEN brings forth a myriad of benefits:

Standardized Integration: A common framework ensures seamless and efficient exchange of data.

Smart Contracts for Automation: Automation streamlines workflows, reducing delays in credit-related processes.

Interoperability and Collaboration: OCEN fosters a connected and dynamic credit ecosystem through interoperability.

Transparency and Reliability: Blockchain ensures a clear and unalterable record of transactions, reducing disputes and establishing trust.

Embracing the Future with OCEN

OCEN, in synergy with Spydra, represents a pioneering leap forward in transforming credit enablement through blockchain innovation. As industries navigate the complexities of the current credit landscape, OCEN emerges as a beacon of collaboration, transparency, and efficiency. Embrace the future of credit enablement with OCEN and be a part of a dynamic, interconnected experience that goes beyond traditional credit solutions.